Taiwan’s telecom sector is poised for rapid expansion as AI-driven demand fuels investment in data centers and cloud services.

The future is shining brighter than ever for Taiwan’s telecom sector. Just a stone’s throw from big-box retailer Costco’s Neihu store stands the brand-new LY2 data center, supporting equipment installations sized like large refrigerators but much heavier at around 2,000 kg/m². The AI servers are connected to major private and consortium submarine cables, which feed Taiwan’s internet and directly link up with Taiwan’s top public clouds.

The LY2 data center became operational in June 2024 under Chunghwa Telecom subsidiary Chief Telecom, which expects the facility to be the only high-specification AI internet data center (IDC) in all of Taiwan until at least 2026. Chief follows a carrier-neutral colocation business model, renting space to client companies for their servers and data service infrastructure.

“2024 was a good year for us, with a 17% year-over-year (YoY) revenue growth rate, reflecting the growing demand of the international cloud and AI service providers for our carrier-neutral IDC colocation, data network, and cloud application services,” said Tim Chiang, Chief’s vice president, in an interview with Taiwan Business TOPICS.

“But this year will be even better, as LY2 will attract more AI customers to set up regional service centers in Taiwan to provide AI application services,” he says. “Taiwan is the best location for service providers to set up network services in the East Asia region.”

Tim Chiang, vice president of Chief, says he expects more AI customers to set up regional service centers in Taiwan.

Tim Chiang, vice president of Chief, says he expects more AI customers to set up regional service centers in Taiwan.

Taiwan currently hosts 27 IDCs owned by seven providers, including Chunghwa, Chief, and the United States’ Zenlayer and Google, with Singapore-based Keppel Corporation planning to launch an AI data center in northern Taiwan in 2026. According to data provided by Asia-focused corporate strategy firm YCP, Taiwan’s overall colocation market revenue is projected to rise from US$175 million in 2025 to US$360 million by 2030, reflecting a strong CAGR of 15.5%, driven by increasing demand for cloud services and AI applications.

Chiang attributes Taiwan’s very high penetration rates for both broadband fixed network access and broadband mobile access and the Taiwan government granting AI-related investment a tax reduction from 2025 to 2029 as the primary drivers of demand. Low regulation is another strong selling point, which has made international content service, cloud service, and AI service providers invest heavily in Taiwan in recent years or are interested in doing so, he says.

Chief entered the carrier-neutral IDC market in 2000. Even though Taiwan’s WTO membership, which it gained in 2002, led to Taiwan opening its telecoms market to foreign operators, the National Communication Commission only allowed them to land their submarine cables and extend their inland lines to the first service node, leaving onward cables to local players and preventing foreign operators from building end-to-end networks. That policy ensured that local providers like Chief remained essential.

“Although some international service providers have their own huge data centers in Taiwan, those data centers only play the role of server farms for computing nodes,” says Chief’s Chiang. “They still need service delivery nodes from Chief to connect to their end customers – like a factory needing a shopping mall.”

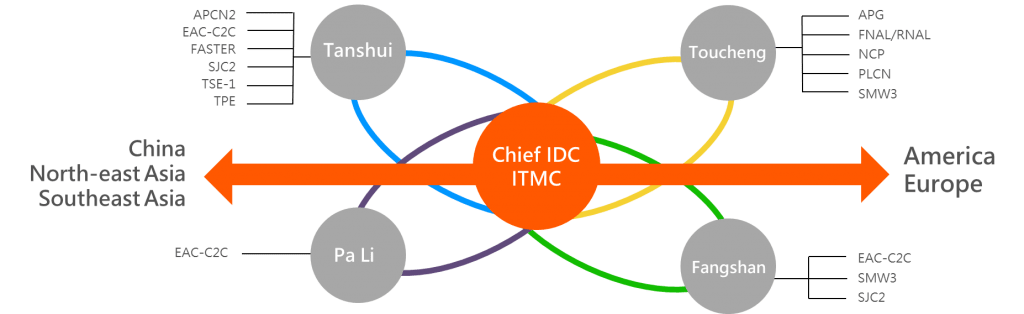

Chief’s three major assets are Chief TPCX (Taipei Cable Exchange), which consolidates consortium submarine cables and private submarine cables in Taiwan, serving as a central hub for international data traffic; Chief TPIX (Taipei Internet Exchange Center), which provides internet traffic exchange service for both international and domestic customers; and Chief CCX (Chief Cloud Exchange), which is Taiwan’s main platform providing cloud direct connect services between customers and the top five cloud service providers, namely AWS, Google, IBM, Microsoft, and Oracle.

Chief TPCX, Chief TPIX, and Chief CCX are connected through a 3-ring fiber network – designed for stability and uninterrupted connectivity – linking all IDCs, every major Taiwanese science and industrial park, and the international fiber ring connecting Taipei to Japan, Hong Kong, Singapore, the Philippines, and other markets.

“If a company has its headquarters in Taichung and wants to avoid the security and reliability risks associated with using public internet, we connect it directly and safely to the likes of Google’s cloud storage and Oracle’s cloud database, as a one-window solution,” Chiang says.

He notes that recent headlines about suspicious vessels cutting Taiwanese submarine cables underscores one of Chief’s advantages. If one cable is cut, Chief can quickly shift the data flow to another by carrying out single window troubleshooting thanks to its supply of the necessary equipment. Chiang predicts that even when three out of Chief’s 14 cables are cut simultaneously, there won’t be any service interruption if the customer has already purchased protection routes from Chief’s submarine cable leasing service.

Gaining the competitive edge

Taiwan is emerging as a leader in the regional data center market by offering strategic advantages despite challenges related to power and land constraints, says Kei Hasegawa, YCP partner and office manager (Hong Kong & Taiwan). The nation’s top competitive factors include its strong semiconductor sector, central location in the regional network, and cost-effectiveness of its operations in a competitive market.

“Taiwan’s globally recognized semiconductor industry led by TSMC contributes more than 60% of the global foundry market, ensuring reliable infrastructure support for high-performance computing and AI-driven data centers,” says Hasegawa.

“Its proximity to major Asian financial and technology hubs – including China, Japan, and Singapore – makes it an attractive destination for data center operations,” he says. “Taiwan also offers a more cost-efficient alternative to Singapore, which had previously imposed a data center moratorium from 2019 to 2022 to restrict new data center developments due to energy consumption and sustainability concerns.”

Hasegawa says the Taiwan government has implemented several policies to foster growth and attract foreign investment in the data center sector. Specifically, the Lai administration approved the Five Trusted Industry Sectors initiative, which provides regulatory incentives and infrastructure support to encourage investment in Taiwan’s semiconductors, AI, military, security and surveillance, and next-generation communications – critical global growth industries that drive demand for data centers.

In addition, the Digital Nation and Innovative Economic Development Program (also known as “DIGI+”) has done its part to create a favorable environment for digital innovation for local and international cloud service providers by supporting a competitive cloud services ecosystem. Notably, DIGI+ – a nine-year program launched in 2017 – helped to maintain Taiwan’s consistent ranking in the World Digital Competitiveness Index, streamlining regulations and promoting cross-border collaboration, which attracted tech giants like Advanced Micro Devices (AMD) to Taiwan. Moreover, the Cybersecurity Act has ensured compliance with global data security standards, making Taiwan a preferred destination for multinational corporations.

“These policies are designed to enhance Taiwan’s digital infrastructure, promote sustainable energy use, and ensure data security, thereby contributing to making the country an attractive destination for data center investments,” says YCP’s Hasegawa.

In terms of telecom equipment, Taiwan’s supply chain primarily focuses on customer premises equipment (CPE) – fiber, Cable DOCSIS, 5G Fixed Wireless Access (FWA), and Wi-Fi routers – while also including contract manufacturing of network infrastructure products like switches and small-cell base stations. According to the semi-governmental Market Intelligence & Consulting Institute (MIC), key Taiwanese manufacturers, such as Accton, Alpha Networks, Arcadyan, Gemtek, Sercomm, and Zyxel, serve as major production partners for leading global telecom operators.

“Demand for telecom equipment is primarily driven by telecom operators’ capital expenditures and the adoption timelines for new technology standards,” says Tzeng Chiau-ling, a senior industry analyst at MIC. “In 2025, as the global economy gradually recovers, broadband infrastructure subsidies in key markets like North America are expected to materialize, driving equipment shipments, while major telecoms and internet service providers will lead the upgrade cycle for next-generation technologies,” she says.

Goodbye price wars

The market started off in 2024 with a reduction in the number of mobile operators, falling from five to three. The previous year, Far EasTone Telecom (FET) had merged with Asia Pacific Telecom (APT), while Taiwan Mobile merged with Taiwan Star.

Even after the mergers, Chunghwa Telecom remains the largest mobile services provider, with 13.12 million subscribers as of end-2023, followed by Taiwan Mobile (10 million) and FET (around 9 million). However, the newly merged companies reported much stronger revenue growth. For example, Chunghwa Telecom’s YoY mobile service revenue growth of 3% in the fourth quarter of 2024 paled in comparison to FET’s YoY mobile service revenue growth of 17.4% in November. Taiwan Mobile, for its part, reported total YoY revenue growth of 10% for the whole of 2024, thanks to the merger’s “ushering Taiwan’s telecom industry into an era of value-driven competition, moving away from the traditional price wars.”

Chunghwa Telecom, headquartered in Taipei, remains the largest mobile services provider in Taiwan, despite changing market dynamics.

Chunghwa Telecom, headquartered in Taipei, remains the largest mobile services provider in Taiwan, despite changing market dynamics.

According to the Economist Intelligence Unit (EIU), the market consolidation in Taiwan reflects a trend of consolidation by private players that it has witnessed in other Asian markets such as Malaysia, Thailand, and Indonesia. “With the market consolidation complete, we expect tariff revisions in 2025, as the existing three companies look to move away from such packages,” says Laveena Iyer, a global technologies, and telecoms analyst at EIU.

“This is often the case in a market with three players. As per industry standards, three to four companies are generally considered optimal for healthy market competition, strong investment in emerging technologies, and affordable tariffs.”

A comparable example is the U.S. telecom industry, which saw a similar consolidation when T-Mobile acquired Sprint in 2020, reducing the number of major mobile operators from four to three: AT&T, T-Mobile, and Verizon. While reduced competition can sometimes lead to higher consumer prices over time, this merger allowed for greater investment in network infrastructure and large-scale upgrades, resulting in expanded coverage and improved network quality for customers.

Iyer says both FET and Taiwan Mobile will also benefit from the spectrum acquired from their smaller merged entities. This will enable cost savings as infrastructure is consolidated, allowing greater investment in expanding and maintaining the 5G network. A similar outcome was seen in the United States when T-Mobile successfully leveraged Sprint’s mid-band spectrum, which accelerated its nationwide 5G rollout and improved network capacity.

However, market consolidation is also subject to criticism. In markets such as the United States and Canada, mergers have led to concerns over higher consumer costs, reduced competition, and job loss. Critics of Taiwan’s telecom mergers similarly argue that fewer players may weaken price competition, though others contend that a healthier industry structure will promote sustainable investment in 5G and AI-driven network expansion.

The European Union has taken a stricter regulatory stance, often blocking telecom mergers that significantly reduce the number of players in the market. Conversely, Taiwan has largely allowed these consolidations, emphasizing the need for stronger industry players to keep up with regional competitors in 5G, AI, and cloud services.

Chinese smartphones gain traction

On the telecom consumer device front, Apple and Samsung have traditionally dominated the Taiwanese market. According to data from Global StatCounter, in October 2024, Apple had a market share of 56.1%, and Samsung had 21.6%, while Chinese brands Oppo and Xiaomi had 6.2% and 3.9%, respectively. The competitive landscape hardly changed between October 2023 and October 2024, which partly reflects the government and consumers’ misgivings around Chinese brands.

“Numerous iPhone OEMs [component suppliers] in Taiwan are well-known among the local populace, further bolstering Taiwanese consumers’ confidence in choosing the iPhone over non-Apple products, and with the decline of HTC, there is currently no iconic Taiwanese smartphone brand, leaving a void in the market,” says Liz Lee of Counterpoint Research, a global market research firm that specializes in technology, media, and telecommunications industries.

“However, in a surprising shift within Taiwan’s competitive smartphone market, Apple gave the top spot to Samsung, with its share slipping to 34% in 2024 after a gradual decline,” she says. “With the discontinuation of 3G network services looming in Taiwan last year, a wave of existing 3G users has upgraded their devices across the year.”

Lee says that thanks to a surge in demand for mid- to low-end smartphones, Samsung has emerged as a primary beneficiary with its Galaxy A series, such as the Galaxy A55 model, which is ranked as the best-selling model.

Nevertheless, Lee notes that Chinese smartphone brands have recently started gaining traction, surpassing HTC in market presence. Last year, Xiaomi (+Redmi) and Vivo also experienced a resurgence, capitalizing on the increased demand for budget-friendly devices. “Along with Oppo, those brands are expected to gradually strengthen their foothold in the region, particularly due to their competitive pricing, which appeals to cost-conscious consumers,” she says.